By David Pring-Mill

The following text has been excerpted from Section 2.1 of the Policy2050 report “Smart Retail: Thematic Analysis — Introducing Innovations to the Retail Sector (2023-2025)” in order to serve as a product sample and fulfill Policy2050’s mission “to keep the most socially-relevant insights outside of any paywall.”

Depending on the use case, emerging retail technologies could represent incremental optimizations or dramatic transformations for retailers. The latter may appear overwhelming, unaffordable, and irrelevant, especially in an economic environment where retailers can witness consumers dropping items in their carts more selectively or even avoiding stores altogether due to sticker shock.

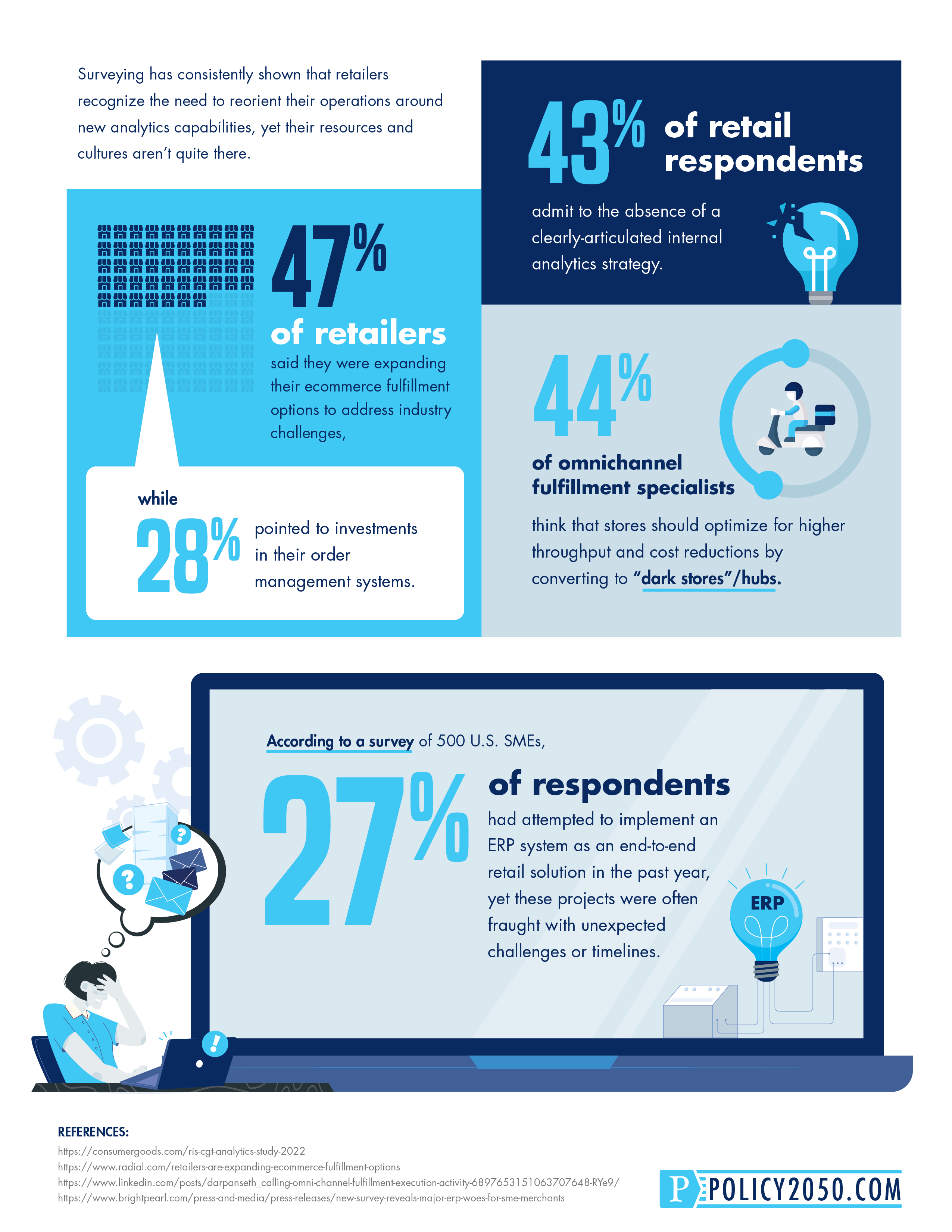

The last Policy2050 Smart Retail report made it clear that major retailers find their own tech stacks and digital cultures to be lacking, which has been directly expressed in retail industry surveys. At the same time, innovative startups aspire to work with them. Why then does technological change in brick-and-mortar feel relatively slow? Why is product/market fit so hard to achieve?

Many leading, digitally-savvy retailers are shifting from digital transformation to digital optimization, typically facilitated by robust data platforms that run cohort analyses and predict consumer behaviors. This enables retailers’ technologists and department heads to tweak the path to purchase and consumer messaging. Part of the decision-making process for a retail VP or internal sponsor involves evaluating the potential downtime and risks of a rip-and-replace project versus something that quickly integrates. With increasing concerns about data security and skepticism about partnerships in which retailers are being used as part of another business’s growth goals, such as in B2B2C scenarios, there may be even more resistance to non-essential technologies and more scrutiny of technology provider incentives.

Based on the name of the trend alone, one might think that “Smart Retail” ought to be a no-brainer – yet surprisingly, sometimes the retail technology ecosystem itself gets in the way of this conceptual realization. In some cases, it’s fairly easy to see how a Smart Retail startup’s innovations – for example, the metaverse – don’t readily map over the current pain points or organizational structures and cultures of major retailers. However, tech ecosystem barriers are perhaps less conspicuous from an outsider’s perspective. On multiple occasions, the large technology providers of retailers’ entrenched legacy systems have thwarted the integrations of newer, perhaps more innovative startups. This contributes to the reluctance to introduce or adopt new technologies along with data-driven strategies that enhance consumer experiences and retail sector value.

Large retail organizations exhibit significant variations in terms of innovation-centric job titles, departments, practices, and KPIs. This lack of uniformity, along with other factors, forces retail technology providers to navigate a complex web of information and relationships in order to determine the best way in. Retailers’ innovation labs may provide a starting point but these labs can sometimes be siloed from the rest of the organization, making them, ironically, the wrong way in for external innovators. Innovation roles and departments often signal transformation and future-proofing without the actual cross-functional follow-through. They may ideate, incubate, and innovate, but do they implement? It depends.

This innovation-centric superficiality may be deemed acceptable, may become progressively meaningful, or may even pose an existential risk, as evidenced by recent store closures and bankruptcies. A more malignant version of the same phenomenon may exist in the form of sustainability-related leadership titles. That has begun to change in recent years; the seriousness or impact of these roles may depend on how central the environmental problem area is to business operations. As the experts interviewed for this report indicated, driving technological adoption and change in large retail organizations is extremely hard, even more so when the area of oversight is largely conceptual, as it can be with innovation or sustainability. Meanwhile, other functions of the organization have a clear P&L as a driver. Therefore, startups need to find the right champion within the retailer’s organization, understand internal processes, and match solutions with defined KPIs.

While small or mid-sized retailers may be more approachable due to the reduced number of decision-makers, they routinely experience significant delays and cost overruns in what are standard, or at least should be standard, ERP projects. Given this baseline, it’s no wonder that innovative retail technologies can sound like infeasible projects to retailers.

However, as retailers reap the rewards of customer-centric investments, their risk appetites and flexibility may gradually change. For example, Walmart remodeled six big-box stores with brighter lights and displays, more elaborate IKEA-esque showcases for discretionary merchandise, mobile content-activating QR codes, and exclusive designer/celebrity/brand partnerships. This effectively transformed these locations into high-performing flagship stores. One analytics firm’s data indicated that visits to the first prototype location eclipsed Walmart’s own baseline by 31.2% and surpassed the average foot traffic of competitor Target by 66.6%.

Consumers appreciate these types of retail innovations, and so they will continue. In the words of Mike Blay, one of Ahold Delhaize’s technology leaders, “If the consumer is not yet ready for a certain innovation, then you are working on a solution for a problem that has not actually arisen yet.”

New Look, a British global fashion retailer, attracted over 238 million visits to its digital properties in 2022 after carefully negotiating and sequencing its IT transformation. The Smart Retail landscape offers a wide variety of capable technological options. Part of the British retailer’s strategy involved steering clear of analysis paralysis and instead identifying the most favorable contractual terms and pricing.

In October 2022, New Look’s CTO Ed Alford, who recently resigned, reflected on his efforts to restore the retailer’s former glory, create a new omnichannel legacy, and carry over an appreciation for strong partnerships, which developed during his time at BP. He said, “In going in and trying to do what we were going to do with New Look, which was a complete technology refresh from the networks to the order management systems, to the store systems, to the payments, the whole thing – I felt that partnerships were going to be really important.”

Despite an industry tendency to underappreciate suppliers or customers, Alford noted that more collaborative, trusting relationships or partnerships can deliver mutual benefits, especially in difficult times. Even internally, Alford said he had been “working with the Chief Procurement Officer to say, look, we could spend six months analyzing and trying to decide between two or three different partners, when actually, any one of them could do the job; it’s just how we set it up. And then, make sure we get the best price.”

This procurement approach shortened lead times and enabled operational agility for New Look. Retail technology providers may disagree with the suggestion that their solutions are interchangeable. However, if retailers don’t recognize their asserted competitive differentiation, it doesn’t matter. This ought to inform which sets of features technology providers emphasize in B2B sales/marketing or which pricing models they present.

As conversations progress, programs are implemented, and results are analyzed, Smart Retail startups will likely adjust their ideal customer profiles and iterate. New information may justify dramatic pivots. Major retailers often value this agility. For example, Scott Donahue, VP of Supply Chain Product at Walmart, has spoken positively about a telematics and fleet management open platform provided by Platform Science, attributing benefits to their “small and scrappy” startup culture. Relatively speaking, that is – Crunchbase measures the startup’s total funding at US$197.7M. Donahue commented, “We had direct access to the CEO, and they were able to pivot quickly when needed.”

Even as the retail sector continues to optimize its pandemic-driven digital transformations, retail technology providers have noticed that the pace of innovation is slowing due to economic concerns and reduced budgets. Retailers remain cautious, especially around experimental technologies that can’t fully prove their ROI. Nevertheless, some consumer behaviors clearly shifted during the pandemic, and retailers will be forced to align with those new habits and expectations. While consumer demand is influential, some innovations are experienced indirectly. For example, retailers may not incorporate a VR or AR experience but if a logistical optimization enables a faster delivery window or increased product availability, consumers are more likely to check out and come back.

The full report “Smart Retail: Thematic Analysis — Introducing Innovations to the Retail Sector (2023-2025)” is now available for purchase on Policy2050.com.